Welcome to this under-the-hood edition where I go down the rabbit hole on interesting businesses, technologies and innovations. We also release a weekly newsletter (The Weekly Signal) showcasing the latest curated signals that caught our attention. Also, fill out the survey so we can deliver the best content to your inbox

52% of our readers are not subscribed, so if you like the content, please double check so you can get the latest updates straight to your inbox. Thanks for reading! 🙏🏼

For a short while, Google looked like the most vulnerable out of all the tech giants.

When OpenAI dropped ChatGPT in late 2022, there were rumblings about what this could do to Google’s entire business model, especially around Search. It was unprecedented.

Here was a product that didn’t just challenge a Google feature; it challenged the very idea of Google. For two decades, Google had been the undisputed front door to the internet. And now, suddenly, there was another door that opened that just didn’t point you to links, but gave you actual answers.

The irony is that it was Google (specifically, the Brain team) that invented the Transformer architecture (which is the “T” in GPT) that currently underpins all of modern AI.

For the actual technical paper itself, you should check out “Attention is All You Need” for the full in-depth dive.

If you want a more visual explanation of how the concept of “Attention” is applied to LLMs, watch this cool video by 3Blue1Brown:

At this point, I think most of us bought into the narrative that Google was going to be challenged and perhaps disrupted. But over the past two years, something remarkable has happened — it turns out that Google wasn’t asleep at the wheel at all. It was building quietly.

Code Red

To understand their comeback, I think you also have to appreciate the crisis.

Google wasn’t just behind; it was culturally paralyzed. The company that pioneered AI research was so cautious about reputational risk and safety that it kept its best work locked in the lab.

The first response from Google’s leadership was pretty frantic, to say the least. In December 2022, a mandate trickled down from leadership to build a ChatGPT rival in just 100 days. The project, which would later become “Bard”, was basically an all-hands deck scramble. Engineers were pulled from every corner of the company to work on it.

When it came time for the big reveal…well, it was kind of shaky. There was a factual error in its very first public demo, which sent Alphabet’s ($GOOG) tumbling, wiping out $100B in market value. You can read one of the articles talking about this during that time — this one is from Investopedia.

But actually, beneath the surface, this whole “Code Red” saga did something crucial for Google – it became a forcing function to eviscerate any of their culture wars inside the org and made them really focused. It ultimately gave Sundar Pichai (CEO) the mandate to smash through all the silos and take educated risks that it had been lacking for years.

Honestly, I think the most important move for Sundar was to fully merge two key AI groups within the company: Google Brain and DeepMind.

The Merge

To fully understand this merger, you have to see Google Brain and DeepMind as two distinct philosophical and cultural entities that just happened to be owned by the same company.

Here’s the quick breakdown of both sides.

Google Brain

Founded: 2011

Key People: Jeff Dean, Greg Corrado, Andrew Ng

Core Philosophy: Pragmatism at a planetary scale

Brain was born out of Google’s infrastructure. Jeff is somewhat of a legendary figure inside (and even outside) Google, who was one of the key architects of the systems that allowed Search, Maps, and Gmail to handle billions of users. The goal was to take the relatively niche (at that time) academic field of deep learning and apply Google-scale engineering to it. The idea was to build AI tools, features, etc., and plug them into Google’s products to make them better.

As mentioned above, this was the group that invented the Transformer, but also things like TensorFlow — their open-source ML framework that allowed developers to build AI products. It democratized AI development, and it became the standard for building deep learning systems. Quick side note: I remember in 2015 working at a startup building computer vision tech, and all the engineers there were just harping on about TensorFlow — it was such a big deal!

Ultimately, for Brain, it wasn’t really about reaching Artificial General Intelligence (AGI), but more about solving real-world problems. They built tools and solved problems that directly benefited Google’s core businesses.

DeepMind

Founded: 2010 (acquired by Google in 2014)

Key People: Demis Hassabis, Shane Legg, Mustafa Suleyman

Core Philosophy: Solve intelligence, and then use that to solve everything else.

DeepMind started in London with a much more audacious goal of building AGI.

These guys became headlines when they built AlphaGo (2016), which was an AI to challenge the best Go player in the world (Lee Sedol), whom it beat. By the way, you should watch the documentary on this.

Their other claim to fame was building AlphaFold (2020), which is arguably their most important achievement. It was able to solve a 50-year-old grand challenge of protein folding by predicting the 3D structure of a protein from its amino acid sequence. Read this article for more information.

Ultimately, DeepMind’s approach was heavily influenced by neuroscience (reinforcement learning). The idea was to create an “agent” (an AI) that learns by trial and error in a simulated environment, guided by a reward signal.

So when Google acquired DeepMind ($500M), one of the best acquisitions in history IMO, a key condition was that it would remain a semi-independent entity, shielded from the product pressures of the main company.

The culture was much more academic and more vision-driven as opposed to the more practical and pragmatic Brain group.

For years, these two groups operated in parallel, usually as rivals. They actually competed for talent and even for computing resources. The internal competition was healthy at times, but it became a threat when OpenAI jumped onto the scene and turned that rivalry into a liability.

So in April 2023, the decision was made: Google Brain and DeepMind would merge to become Google DeepMind, led by Demis Hassabis. The goal was to unify both sides with a clear mandate: build the AI models that would not only compete with OpenAI but even surpass them.

Here was the announcement from Sundar back in 2023.

The first real product from the merger was Gemini. It was built from the ground up to be multimodal, combining the best of both worlds: the massive scale and data processing power from Brain with the reasoning and planning that came from DeepMind.

Enter Gemini

After a series of rapid-fire releases in 2023 and 24, Google has quickly inched its way back to the forefront alongside OpenAI and many others.

Gemini’s superpower is its context window.

You can think of a context window as the AI’s memory. It’s the amount of information it can look at in a single go. For a long time, this was a huge bottleneck. Now, chasing these larger context windows is becoming an arms race. It means you can drop an entire book, dense financial report, or hours of video transcript into the AI and ask it to reason across the whole thing at once.

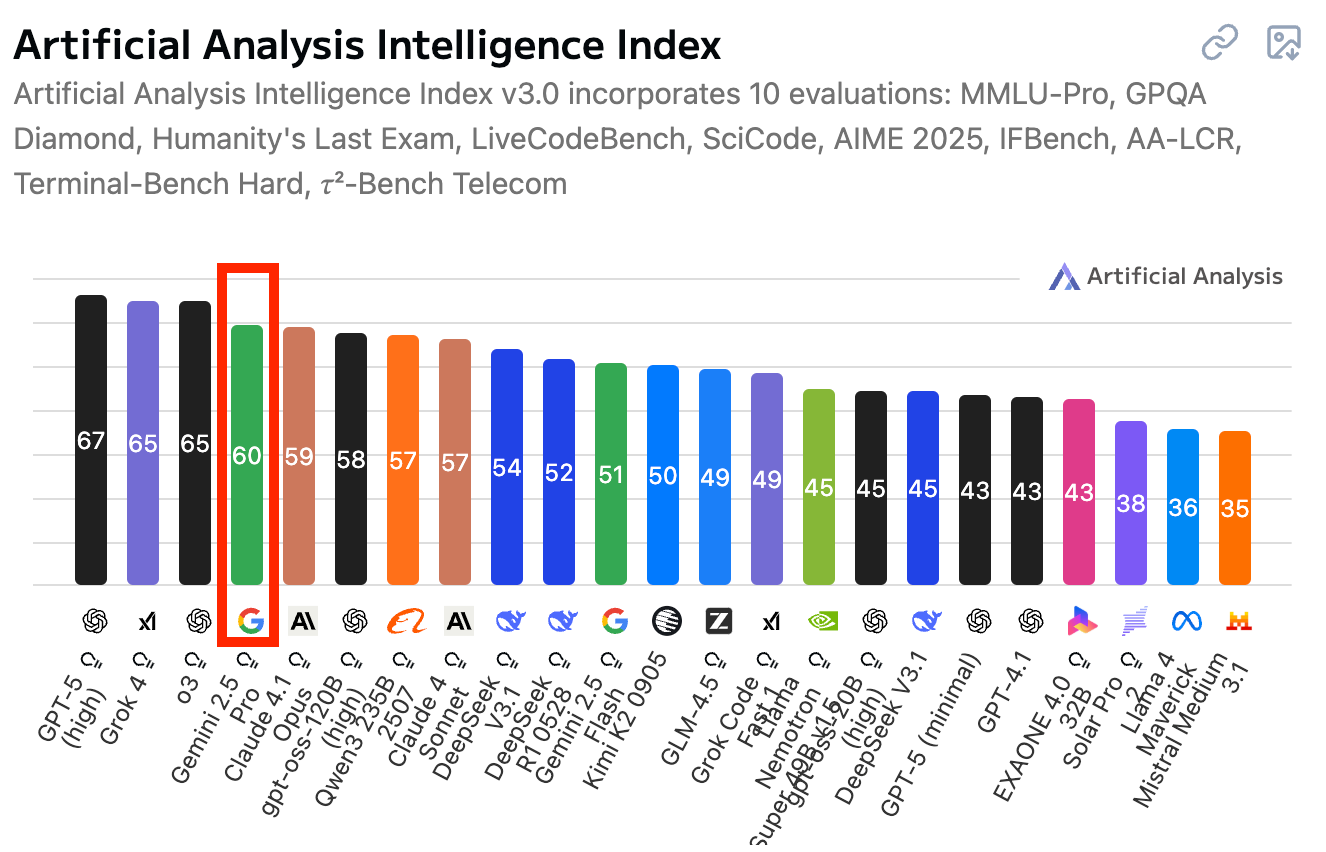

As of September 2025, you can see how quickly Google has been able to catch up, just trailing behind ChatGPT-5 and Grok 4 in just two years.

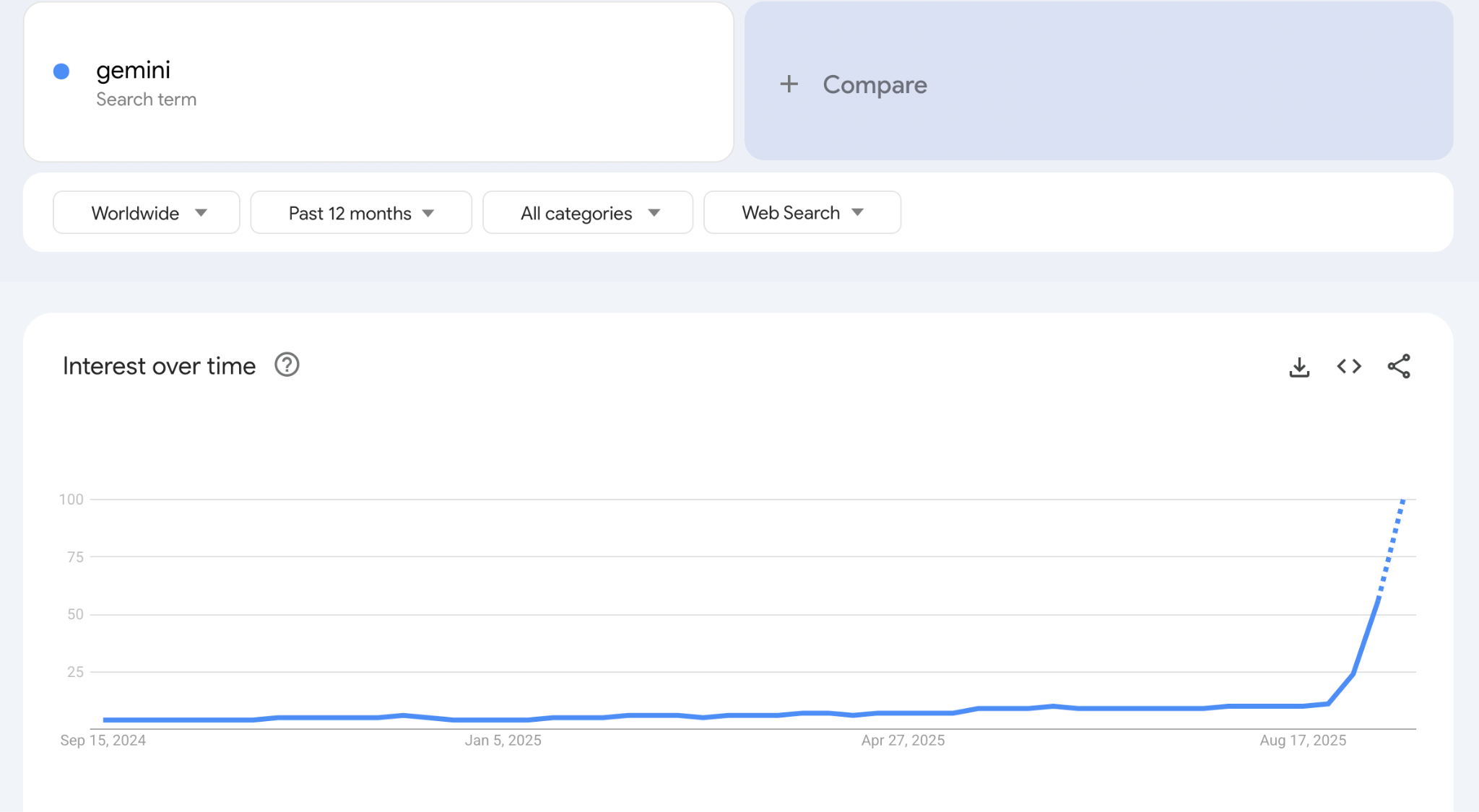

Also, another interesting observation: the “gemini” keyword is on the rise according to Google’s keyword trends. It’s fair to say that it’s entering the zeitgeist alongside ChatGPT and becoming one of those generational products.

Time will tell how long this lasts.

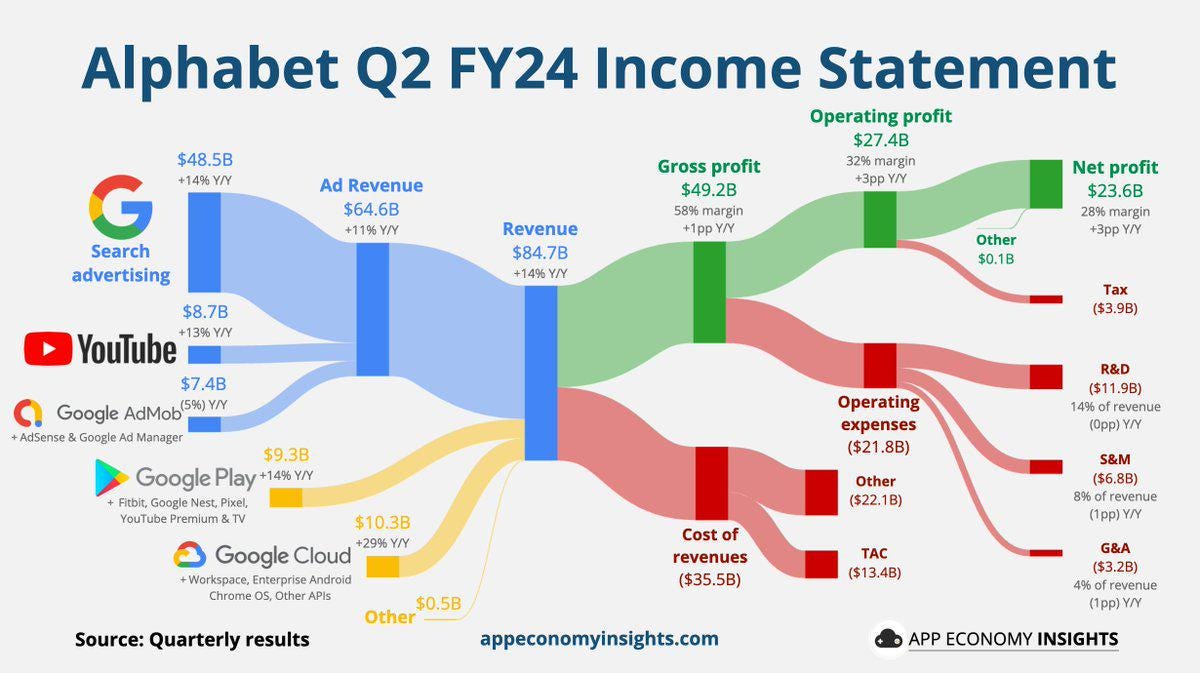

GCP’s Rise

Another aspect of Google’s comeback is its Google Cloud Platform (GCP).

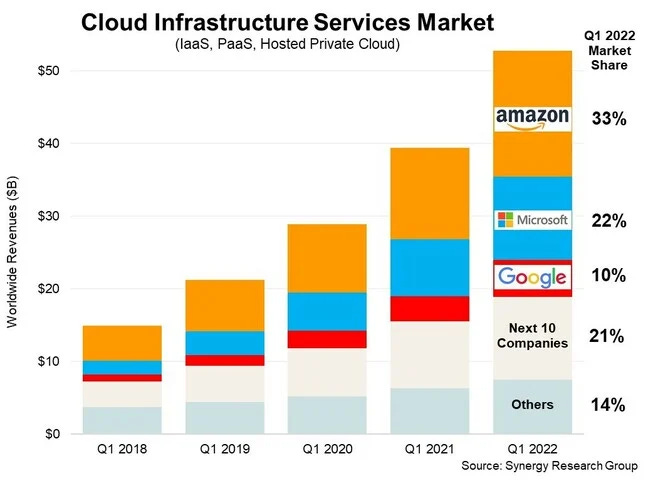

While everyone was fixated on AI chatbots, a much bigger story was happening, which was the rise of GCP. For years, GCP was seen as coming in third place in the cloud wars, trailing far behind Amazon’s AWS and Microsoft Azure. But under the hood, it was building multiple engines of revenue.

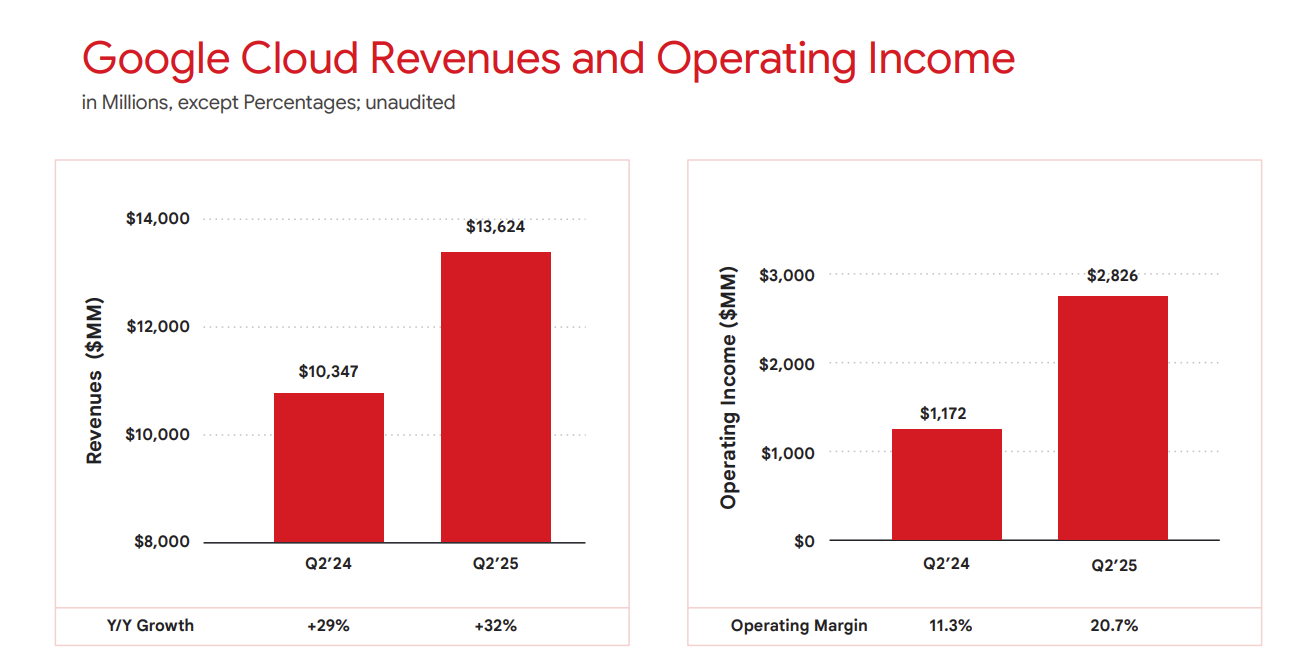

Over the past few years, Google has built a world-class cloud platform and then supercharged it with its AI. While AWS was the incumbent and Azure had the enterprise distribution, Google had the best AI tools that integrated seamlessly with its own core products. When the generative AI boom hit, companies flocked to the platform that could best help them build their own AI applications.

If you look at the revenue jump in the visual below, it’s a clear statement that Google is tripling down on GCP to be more robust and feature-rich alongside AI. If you use Google Workspace, you can already start to see Gemini being integrated throughout the entire ecosystem, from Gmail and Google Drive, all the way to how you deploy apps on the Cloud itself.

AWS still has the lead, and probably will continue to do so into the foreseeable future, but Google isn’t playing around anymore, and it could come for their market share.

It’s crazy to see that even with such absolute revenue numbers in Cloud, it still pales in comparison to their ad revenue. Nonetheless, over the next few years, that yellow stream will only get fatter.

Waymo

For the better part of the decade, Waymo, Google’s self-driving car project, was the ultimate “moonshot”.

It was always five years away, burning billions of $$$ a year. It was kind of easy to dismiss it as another one of Google’s interesting but commercially unviable projects…until it wasn’t.

Another side note: I used to ride my bike via the Waymo Campus (it’s a few miles from the main Google campus) on the way back home from work, and would always see a fleet of Waymos parked on their lot. This was 2015 and 16. I also noticed that Waymos were always in “test” mode, collecting data on some of the main roads in the Bay Area – who knew that would actually come to this!

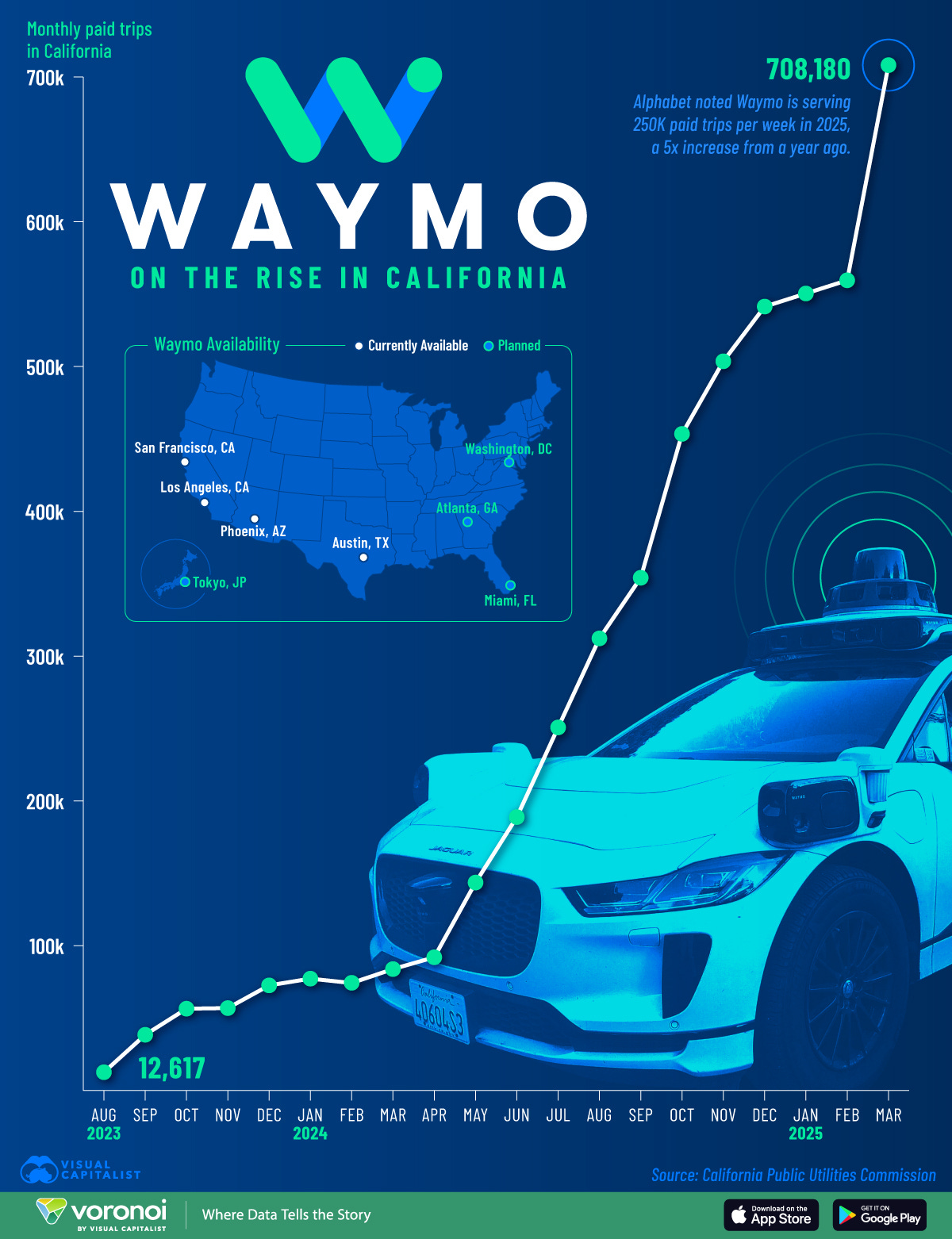

Over the past 18 months, Waymo has hit an inflection point. It has gone from a limited service in Phoenix to a full-blown commercial operation that is scaling at a crazy pace.

Here are a few fun facts for you:

Rapid City Expansion: Waymo is now fully operational in Phoenix, San Francisco, Los Angeles, Austin, and Atlanta. It's actively expanding to Dallas, Denver, and Seattle, with Miami and Washington D.C. on the roadmap for next year. It's even launching its first international service in Tokyo.

Stealing Market Share: In San Francisco, Waymo has already captured an estimated 17% of the rideshare market from Uber and Lyft in the areas where it operates.

Hitting Scale: The service now provides over ~200,000-250,000 paid rides per week.

This is not a test anymore; it’s a land grab, and it’s building a real, functioning transportation network.

Waymo has proven its tech is safer than human drivers, and now it’s focused on scaling its fleet and driving down costs.

Waymo is one of the few aces up Google’s sleeve. It’s a multi-trillion-dollar market, and Google already has a 10-year head start. But there is big competition on the horizon: Tesla’s Robotaxi has already launched, Amazon Zoox is ramping up, and even Uber is coming back to the table to have a crack at it again.

If you’re ever in one of these cities, you should try it out. Be sure to download the Waymo app, and it’s as easy as booking an Uber.

The Road Ahead

It looks like Google (and by extension Alphabet) has this one in the bag.

But like in any business, there’s always going to be setbacks, challenges, and problems to fix. Google is heading in the right direction, but as already shown above in the revenue stream visual, Google’s empire still depends on its search and advertising business, which is currently under threat.

Browsers

In this case, the threat doesn’t just come from other chatbots. It comes from a new breed of AI-native browsers. One prime example is Perplexity’s Comet browser, which is built from the ground up to answer questions directly, summarize web pages, and automate tasks. So instead of typing a query into Google, you just ask the browser a question.

This is a profound shift because it attacks the very foundation of Google's ad-supported business model. If users get their answers from the browser itself, they never see Google’s search results page, and they never click on the ads that generate the vast majority of their revenue.

Google knows this is an existential threat. It's probably why they are aggressively integrating AI Overviews into their own search results — called Generative Engine Optimization (GEO).

The new game isn't about getting a click; it's about getting cited. When a user asks a question to an AI like Gemini, the model doesn't just show links. It synthesizes information from multiple sources and delivers a direct, comprehensive answer.

It’s fair to say Chrome has been woefully under-innovated, and others are taking the lead.

The Innovator’s Dilemma

It’s a concept coined by Clayton Christensen, and it basically describes how successful companies can fail by doing everything "right." They listen to their customers, invest in their most profitable products, and end up being blindsided by a disruptive new technology that initially looks inferior or less profitable.

This is Google's situation in a nutshell:

Cash cow: Google's search advertising business is one of the most profitable enterprises in human history. Every decision is made to protect and grow this massive revenue stream.

Disruptive tech: Generative AI search is the disruption. In its early stages (think of Bard's flawed debut), it looked less reliable and less profitable than the classic "blue links" model. So why would Google aggressively push a product that gives the user the answer directly, when its entire business is built on getting them to click on ads on the way to the answer?

Cannibalization fears: If Google goes all-in on generative AI search (which they are now being forced to do with "AI Overviews"), they risk cannibalizing their own advertising revenue. Every search that ends in a zero-click, AI-generated answer is a potential lost ad click. Publishers are already reporting significant drops in referral traffic.

Competitor's advantage: Newcomers like Perplexity have nothing to lose. They can build the best possible "answer engine" from the ground up without worrying about disrupting an existing business model.

Google is now in the unenviable position of having to disrupt itself. They have to build the AI-powered future of search that could potentially kill their golden goose, because they know if they don't, someone else will

Another Ace: TPUs

But all hope isn’t lost. There is another ace that Google could use.

Outside of NVIDIA, there hasn’t really been anyone to tackle the GPU moat they’ve held for such a long time. The reason they’re worth $4T+ is because everyone keeps flocking to them for compute. But Google has been quietly building TPUs (Tensor Processing Units) for itself. TPUs are Google’s answer to GPUs — they are basically an ASIC (Application Specific Integrated Circuit) that does everything a GPU does and then some.

Now, Google is beginning to provide Infrastructure-as-a-Service (IaaS) of their TPUs to Anthropic and xAI. If Google ever spun out TPUs + DeepMind, the business itself could be worth around $900B!

The reason NVIDIA has been able to dominate isn’t just because of their chips; it’s also their easy tooling, cloud distribution, and entire ecosystem. So if Google shrinks the gap on this, then it could really do some competitive damage to NVIDIA.

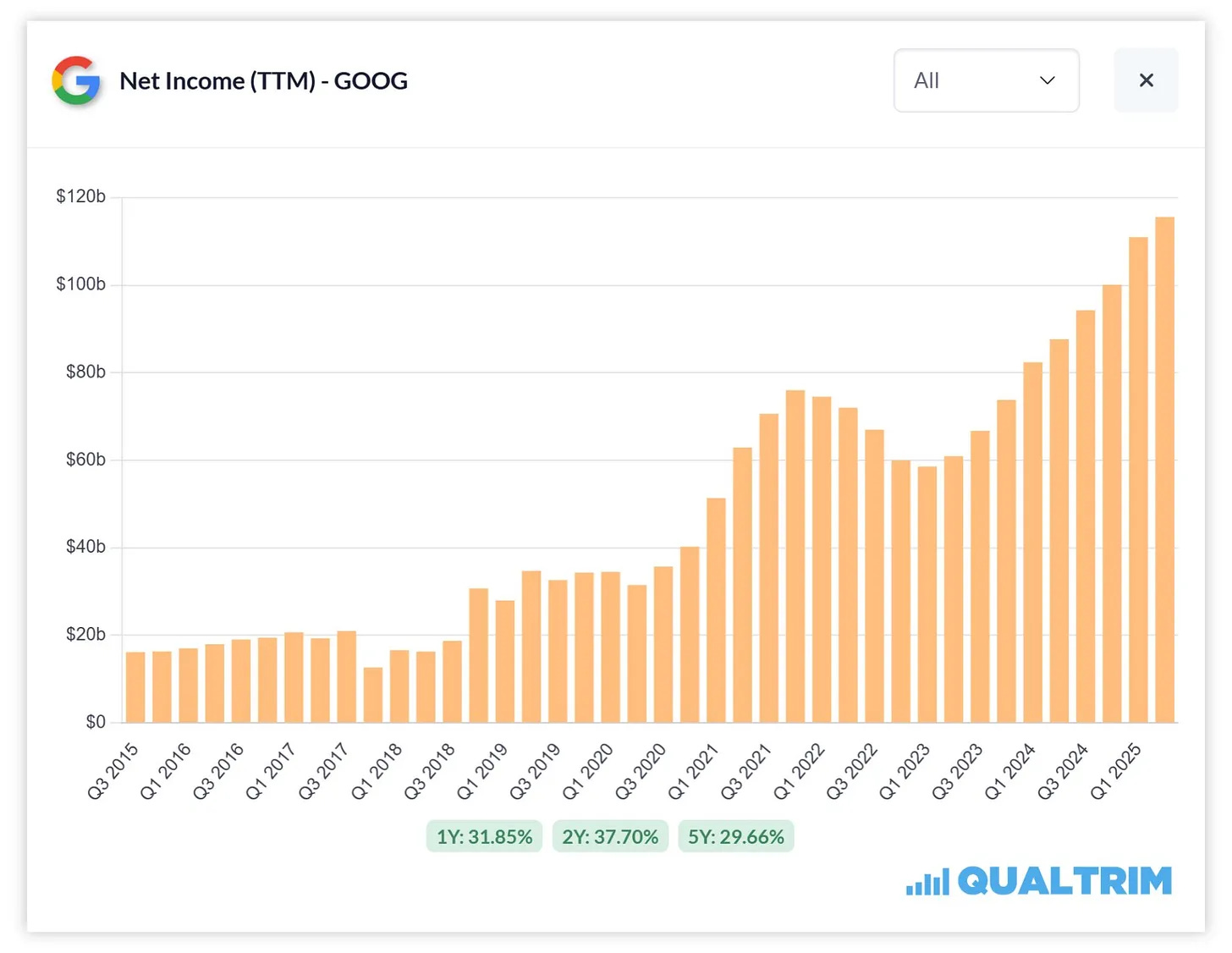

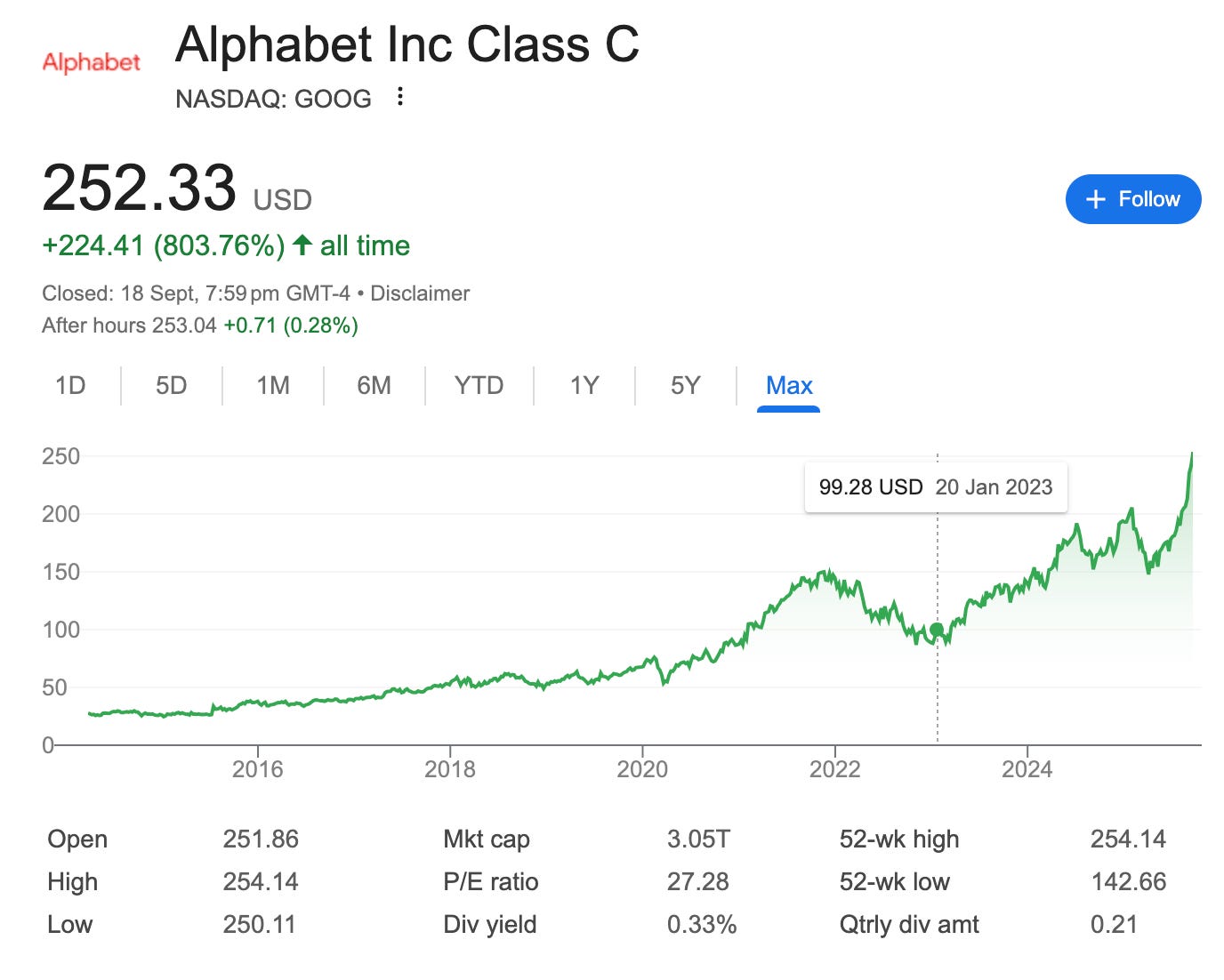

At the end of the day, don’t feel too sorry for Google’s challenges and struggles. Their stock is at an all-time high as of the writing of this piece. They’ll do just fine.

If you liked this, please consider subscribing and sharing it. Thanks for reading until the end.

Here are a few more popular posts you might enjoy:

🙋🏻♂️ Survey

To build the best newsletter for you all, I’d love to get some feedback. If you have some time, please fill out the following survey.

🤩 Deals, Discounts & Affiliates

You can find carefully selected offers and deals here.

🙏🏼 Connect with Me

Are you new to the newsletter? Subscribe Here

Check out my YouTube channel (and subscribe!)

If you’re a founder, apply here (Metagrove Ventures) for startup funding or contact me directly at barry@metagrove.vc

If you think this could be helpful and informative to others, please share it :)

Thanks for reading, and see you next week!

Barry.